First-Time Homebuyer? Don’t Make These 6 Common Mistakes!

Buying your first home is one of the most exciting milestones in life, but it can also be overwhelming. The process is filled with decisions that could impact your financial future, and as a first-time homebuyer, it’s easy to make mistakes along the way. As an experienced realtor, I’ve worked with many first-time buyers, and I’ve seen the common pitfalls that can turn the excitement of homeownership into unnecessary stress or financial strain.

To help you navigate the home-buying process smoothly, here are six common mistakes first-time homebuyers should avoid—and how to make sure you don’t fall into these traps.

1. Not Getting Pre-Approved for a Mortgage

One of the biggest mistakes first-time buyers make is not getting pre-approved for a mortgage before starting their home search. Without a pre-approval, you won’t have a clear understanding of how much you can afford, and this can lead to unrealistic expectations or wasted time looking at homes that are out of your budget.

A mortgage pre-approval is a process where a lender evaluates your financial situation, including your income, credit score, debts, and assets, to determine how much they are willing to lend you. The pre-approval process gives you several advantages:

- Knowing your budget: You’ll have a clear idea of your price range, helping you focus on homes you can afford.

- Demonstrating seriousness: Sellers often prefer buyers who are pre-approved because it shows you’re serious and financially prepared to buy.

- Avoiding disappointment: Without pre-approval, you could fall in love with a home only to find out you can’t get the loan to buy it.

To avoid this mistake, make sure to speak with a lender and get pre-approved before you start shopping for homes. This will not only give you confidence in your budget but also make you more competitive in the market.

2. Focusing Only on the Monthly Payment

When buying a home, many first-time buyers focus solely on the monthly mortgage payment, overlooking the other costs associated with homeownership. While it’s essential to ensure that the monthly payment fits into your budget, it’s equally important to consider the full scope of expenses.

Here’s what you need to account for beyond your mortgage payment:

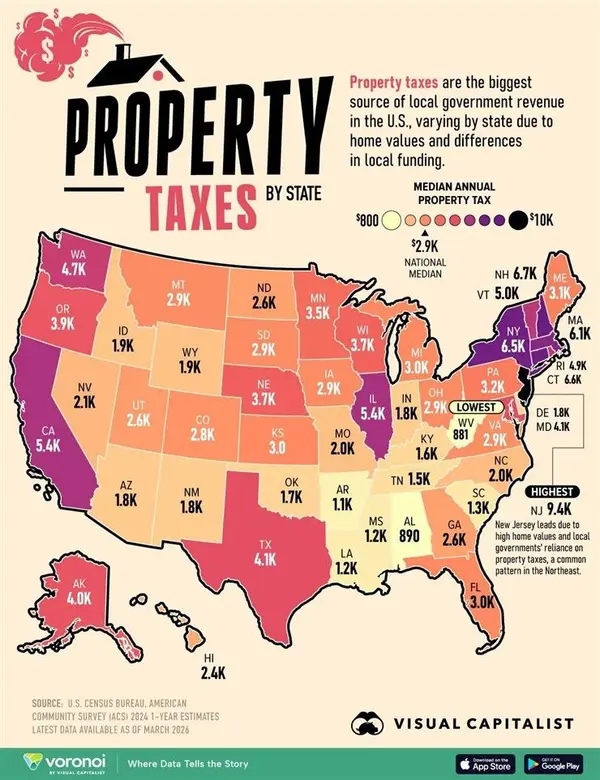

- Property taxes: Property taxes vary by location and can add a significant amount to your monthly housing costs.

- Homeowners insurance: You’ll need to budget for insurance to protect your home from damage or loss.

- Private mortgage insurance (PMI): If you’re putting less than 20% down, you’ll likely be required to pay PMI, which protects the lender if you default on the loan.

- Home maintenance: As a homeowner, you’re responsible for maintaining your property, including repairs, landscaping, and general upkeep. Experts recommend setting aside 1-3% of the home’s purchase price annually for maintenance.

- Utilities: Utility costs, including water, electricity, gas, and trash removal, can vary widely depending on the size of the home and its location.

By considering all these factors, you’ll have a more realistic understanding of what homeownership will cost, helping you avoid financial strain down the road.

3. Skipping the Home Inspection

In the excitement of finding your dream home, you might be tempted to skip the home inspection, especially if you're trying to close quickly. However, skipping the home inspection is one of the costliest mistakes first-time buyers can make.

A home inspection is a comprehensive evaluation of the property’s condition by a certified inspector. It covers everything from the foundation and roof to the plumbing and electrical systems. Here’s why it’s so important:

- Uncover hidden issues: Even homes that look flawless on the surface can have underlying problems, such as faulty wiring, plumbing leaks, or roof damage. These issues can be expensive to fix if left undiscovered until after you’ve closed the deal.

- Negotiation tool: If the inspection reveals problems, you can use the findings to negotiate repairs or a price reduction with the seller.

- Peace of mind: Knowing the condition of the home gives you peace of mind that you’re making a sound investment.

I always recommend that buyers invest in a professional home inspection. The relatively small cost of the inspection is well worth the protection it provides against costly surprises down the road.

4. Not Considering the Future

Many first-time buyers get caught up in their immediate needs and desires, focusing on what they want right now without thinking about the future. While it’s important to find a home that suits your current lifestyle, it’s also essential to consider your long-term plans.

Here are a few questions to ask yourself when thinking about the future:

- Will the home meet your needs in 5-10 years? If you plan to start a family, will the home still be suitable as your family grows?

- Is the location desirable for long-term living? Consider the quality of the local schools, the neighborhood’s development potential, and the proximity to work, family, or recreational activities.

- Will the home appreciate in value? It’s crucial to think about the home’s resale potential. Look for properties in neighborhoods that are stable or up-and-coming, as they are more likely to appreciate over time.

Buying a home is a long-term investment, and considering your future needs will help you make a smart choice that you won’t regret in a few years.

5. Making an Emotional Decision

Buying your first home is an emotional experience, but one of the biggest mistakes first-time buyers make is letting their emotions drive the decision. It’s easy to fall in love with a house because it has a beautiful kitchen or a spacious backyard, but making a purchase based purely on emotion can lead to poor financial decisions.

Here’s how to keep emotions in check:

- Stick to your budget: Don’t stretch yourself financially just because you “must have” a particular home. Remember, you’re not just buying a house—you’re buying a mortgage, and stretching your budget could leave you financially vulnerable.

- Be objective: Focus on the home’s condition, location, and long-term potential. Does it meet your needs and offer good value for your money?

- Sleep on it: If you’re feeling unsure, give yourself time to reflect before making an offer. Don’t rush into a decision just because you’re worried about missing out.

Buying a home is one of the largest financial commitments you’ll ever make, so it’s essential to keep your emotions in check and make a decision based on facts and careful consideration.

6. Draining Your Savings for the Down Payment

While saving for a down payment is a crucial part of buying a home, many first-time buyers make the mistake of using all their savings for the down payment and closing costs, leaving themselves with little to no financial cushion.

It’s important to have money set aside for emergencies and unexpected expenses, especially once you become a homeowner. Homeownership comes with its own set of costs, including repairs, maintenance, and even surprise expenses like a broken water heater or a leaky roof.

To avoid this mistake, here’s what you should do:

- Create a budget: Make sure you leave enough money in your savings account to cover three to six months of living expenses. This will give you a financial buffer in case of emergencies.

- Consider lower down payment options: If putting 20% down will drain your savings completely, explore loan programs that allow for lower down payments, such as FHA loans (which require as little as 3.5% down) or VA loans (which require no down payment for eligible veterans).

- Factor in closing costs: Remember that closing costs can range from 2% to 5% of the purchase price, so make sure you budget for those as well.

A healthy savings account will give you peace of mind as you transition into homeownership, ensuring that you’re prepared for any unexpected costs.

Conclusion

Buying your first home is an exciting milestone, but it’s also a complex process filled with potential pitfalls. By avoiding these six common mistakes, you’ll be better equipped to make smart decisions that set you up for long-term success as a homeowner.

Remember:

- Get pre-approved for a mortgage before you start shopping.

- Consider the full cost of homeownership, not just the monthly payment.

- Never skip the home inspection—it’s your best protection against costly surprises.

- Think about the future when choosing a home to ensure it meets your long-term needs.

- Keep your emotions in check and make decisions based on facts, not feelings.

- Don’t drain your savings for the down payment—leave yourself a financial cushion for emergencies.

By following these guidelines and working with an experienced realtor, you can navigate the home-buying process with confidence and turn the dream of homeownership into a reality.

If you’re ready to start your home-buying journey, I’m here to help! As an experienced realtor, I can guide you every step of the way. Contact me today at (770) 401-1448 or visit paulmcparland.com to get started on finding your dream home!

Categories

Recent Posts

"Whether buying or selling a home, my #1 job is to advise my clients so they optimize their largest financial investment while avoiding any pitfalls that could cost them tens of thousands of dollars. "